LOG IN

LOG IN

Pension Salary Sacrifice: Benefits, Drawbacks, and What Changes in 2029

Prompted by the recent enhancements to the MyFinanceFuture Planner to incorporate changes to pension salary sacrifice announced by the Chancellor in the last Budget, this article gives you what you need to know about saving into a pension via salary sacrifice — and how the Budget changes affect the strategy.

Content

- Why is saving into a pension by salary sacrifice a good thing?

- What are the downsides compared to other investments, like ISAs?

- How does the benefit of salary sacrifice vary by income level?

- What's changing as a result of the Budget?

- Why did the government introduce the changes?

- How will salary sacrifice work in practice after April 2029?

- How do the changes affect the numbers at different income levels?

- What should you consider doing differently before and after the changes?

- Final thoughts: will salary sacrifice still be worth it?

Why is saving into a pension by salary sacrifice a good thing?

Workplace pension saving is one of the most tax-efficient ways to build long-term wealth — and salary sacrifice adds further advantages on top of the standard benefits.

General benefits of workplace pension saving

- Matched Employer contributions add “free money” on top of your own savings that you would not otherwise receive.

- Tax relief at your highest marginal rate — anywhere from 20% to an effective 60% depending on your earnings — makes pensions one of the most powerful tax-efficient savings vehicles available.

- Child Benefit savings: if your income is between £60k–£80k and you have children under 18, pension contributions that reduce your adjusted net income can reduce or eliminate the Higher Income Child Benefit Charge.

- Childcare savings: if you earn over £100k and have young children, pension contributions that bring adjusted net income below £100k can unlock funded childcare worth up to £13,000 per year per child.

- Tax-efficient growth: pension funds grow largely free of income tax and capital gains tax, meaning more of your investment return compounds over time.

- Higher contribution limits: you can contribute up to £60,000 per year into a pension (subject to earnings), compared to a £20,000 annual ISA limit.

- Ease of saving: auto-enrolment and payroll deduction make pension saving automatic and low-effort, supporting consistent long-term wealth building.

Additional benefits specific to salary sacrifice

- You avoid paying Employee National Insurance (NI) on contributions — worth up to 8% of the amount contributed depending on your earnings.

- Your employer avoids Employers' NI, saving 15% of the contribution — many employers share this saving with employees through enhanced pension contributions.

What are the downsides compared to other investments like ISAs?

Pensions are not suitable for every savings goal, and salary sacrifice in particular introduces some trade-offs worth understanding before you commit.

General drawbacks of pension saving

- Locked-in funds: pension money is inaccessible until at least the Normal Minimum Pension Age (currently 55–57), making pensions unsuitable for emergency funds or medium-term goals.

- Tax risk in retirement: if you expect to pay a higher rate of tax in retirement than now, heavy pension saving may be less efficient. A balanced mix of pensions and ISAs supports better tax planning.

- Rule changes: governments have changed pension and tax rules repeatedly in recent years and may do so again, affecting when and how you access your pension and how withdrawals are taxed.

Specific drawbacks of salary sacrifice

- Lower contractual salary: salary sacrifice reduces your headline salary, which can reduce employment benefits linked to pay, such as life cover, income protection, and employer sick pay.

- Mortgage affordability: some lenders base borrowing limits on basic salary, so a lower contractual salary can reduce how much you can borrow — though some lenders do assess affordability on pre-sacrifice salary or net disposable income.

- Low earners may be limited in the extent to which they can sacrifice salary by enforcement of minimum salary levels (e.g. minimum wage), or find doing so takes them below thresholds for building State Pension qualifying years or for statutory maternity pay.

- Very high earners (over £200,000) need to consider how salary sacrifice interacts with the annual allowance taper, which differs from standard pension contributions and may be less beneficial in some cases.

How does the benefit of salary sacrifice vary by income level?

Not everyone gains equally from pension saving or salary sacrifice — the relative benefit depends significantly on your income, tax position, and personal circumstances.

Who benefits most from pension saving in general

- Those earning just over £100k get the greatest short-term benefit, since pension contributions can restore the personal allowance (withdrawn between £100k–£125,140), effectively delivering 60% tax relief — and may also unlock funded childcare worth up to £13,000 per child per year.

- Those earning just above the Higher Rate threshold (£60k) benefit from 40% tax relief and, if they have dependent children, may be able to reduce or eliminate the Higher Income Child Benefit Charge.

- For all other savers, the choice between pensions and ISAs is more nuanced and depends on individual tax positions both now and in retirement — in particular, the "tax-rate arbitrage" between tax avoided on contributions today versus tax paid on withdrawals later.

- Cashflow planning tools that model your finances and tax position over your lifetime can help inform how much to allocate to pensions versus other investments.

Who benefits most from salary sacrifice specifically

- Employees whose employers share a significant portion of the Employers' NI saving — for example, a £5,000 sacrifice could become £5,750 in pension contributions once the employer passes on their 15% NI saving.

- Basic Rate taxpayers tend to see a proportionally larger Employee NI saving, since the full 8% NI rate applies to earnings below the upper earnings limit (£50,270).

- Those with long horizons to retirement, for whom even a few hundred pounds of additional annual contributions compounds substantially over decades.

Who benefits least

- Those who expect to be in a higher tax band in retirement than they are now — for example, Basic Rate savers who anticipate high spending in retirement that pushes withdrawals into the Higher Rate band.

- Those who have already accumulated significant pension savings (projected to exceed around £1m by retirement), for whom the benefit of further pension saving is restricted by the Lump Sum Allowance (LSA), which limits availablity of further tax-free cash on withdrawal.

- Earners above £200k and those who have already started drawing their pension, who face lower annual allowances.

- Very low earners near or below NIC and income tax thresholds, who may get little or no NI or tax advantage from salary sacrifice.

- Employees whose employers retain all NI savings, limiting the gain to the employee's own NI saving and standard tax relief only.

What's changing as a result of the Budget?

Last autumn's Budget introduced a cap on the NI exemption for salary sacrifice pension contributions, taking effect from April 2029.

- From 6 April 2029, the amount of salary sacrifice pension contributions exempt from NICs will be capped at £2,000 per tax year per employee, rather than being unlimited as it is today.

- Contributions via salary sacrifice above £2,000 will still be permitted, but the excess will be subject to both employee and employer NICs — as if it were a normal pension contribution made from take-home pay.

- Income tax treatment does not change, and there is no change to the unlimited NI exemption on employer pension contributions made outside salary sacrifice.

Why did the government introduce this cap?

The government's decision to cap the NI exemption was driven by cost, fairness, and the desire to target relief more precisely at lower and middle earners.

- Fiscal impact: the NI relief on salary sacrifice was becoming increasingly concentrated among higher earners making large contributions or sacrificing bonuses. The Office for Budget Responsibility estimates the cap will raise around £4.7bn in 2029–30 and £2.6bn in 2030–31.

- Perceived fairness: the change aims to reduce the disparity between employees with access to generous salary sacrifice schemes and those without.

- Targeted relief: the government stated it wants to preserve NI benefits for low and middle income workers, while curbing reliefs that "relate disproportionately" to higher income pension savers.

- The cap allowed the government to raise revenue without increasing headline NI or income tax rates.

How will salary sacrifice work in practice after April 2029?

The impact of the cap will vary considerably depending on how much you currently sacrifice and how your employer responds to the change.

- If you sacrifice £2,000 or less per year, salary sacrifice will work almost exactly as it does today — full NI and tax advantages continue to apply on that amount.

- If you sacrifice more than £2,000 per year, the additional NI cost will reduce your take-home pay, or you will need to reduce your sacrifice to maintain the same net pay.

- Employers may redesign their schemes: some may continue to share a proportion of their NI saving on the first £2,000 only; others may reduce or remove NI-based uplifts entirely, particularly for higher earners where the employer now pays NIC on contributions above the cap.

- High earners and their advisers are likely to use salary sacrifice up to the £2,000 NI-free limit, then explore other routes — such as standard personal contributions, investing a bonus, or ISAs.

- Providers expect the changes to reduce pension fund outcomes for some employees over time, as total contributions (after accounting for lost NI savings) may fall unless individuals choose to offset the change.

How will the cap affect the numbers at different income levels?

To make the impact concrete, here is how the annual benefit of salary sacrifice changes for three different taxpayer groups — before and after the £2,000 cap.

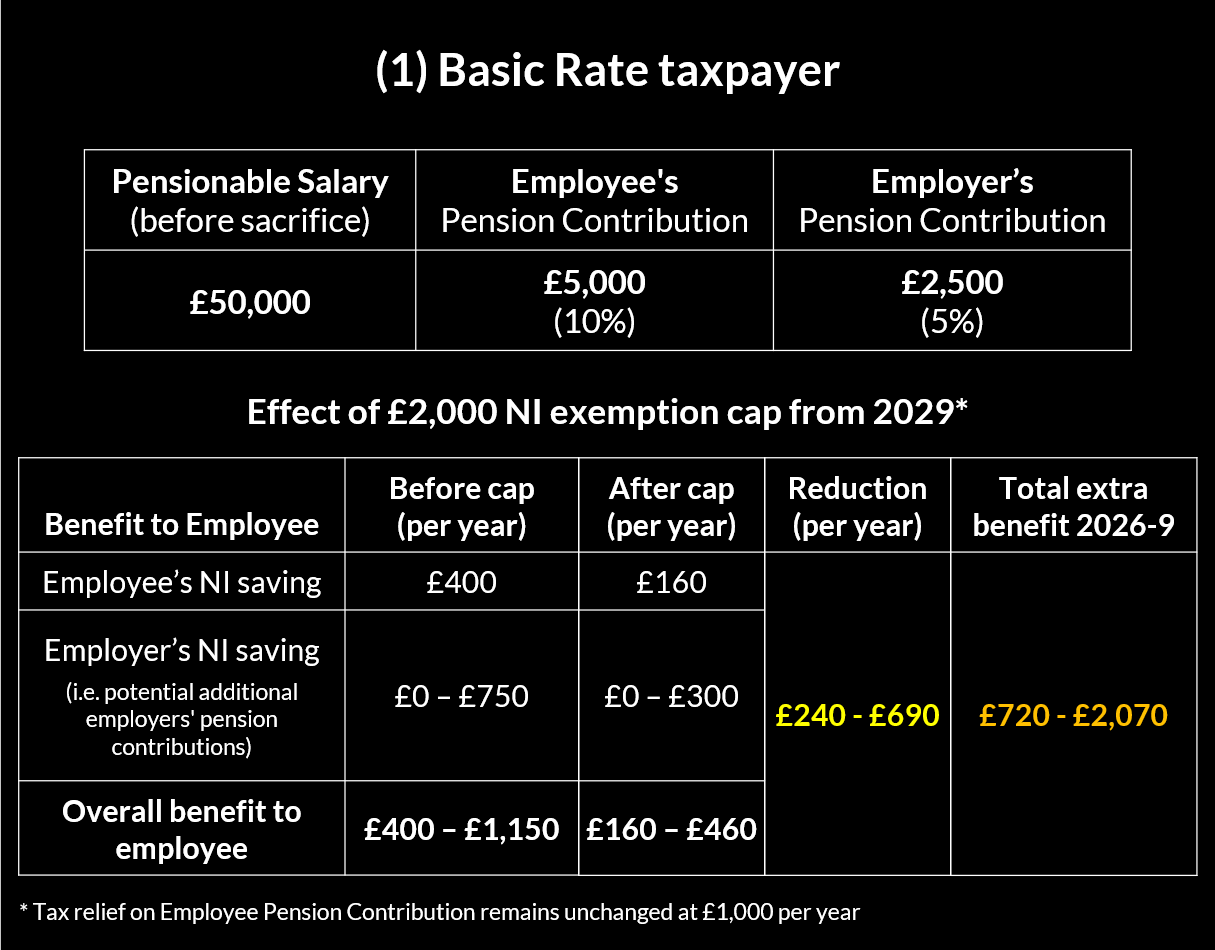

- Basic Rate taxpayer (£50,000 pensionable salary, contributing 10% with a 5% employer contribution): the current annual benefit of salary sacrifice over standard pension saving is up to £1,150 — comprising £400 in Employee NI saving and up to £750 in additional employer contributions (depending on how much of the Employers' NI saving is shared). After 2029, this falls to up to £460 (£160 Employee NI saving plus up to £300 from the employer).

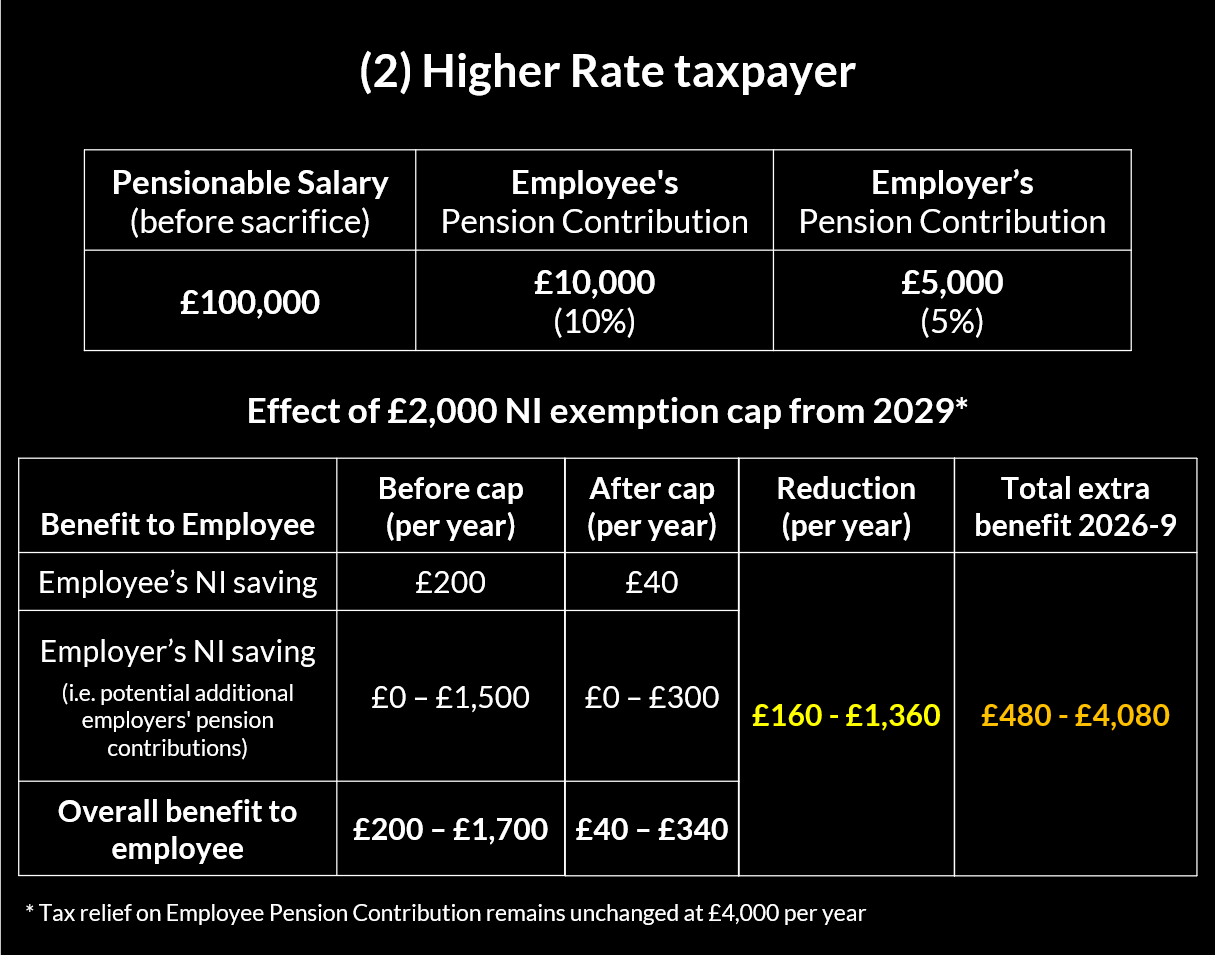

- Higher Rate taxpayer (£100,000 pensionable salary, contributing 10% with a 5% employer contribution): the current benefit is up to £1,700 — with only £200 from Employee NI (since the rate above £50,270 is just 2%) but up to £1,500 from Employers' NI sharing. After 2029, the benefit falls to up to £240.

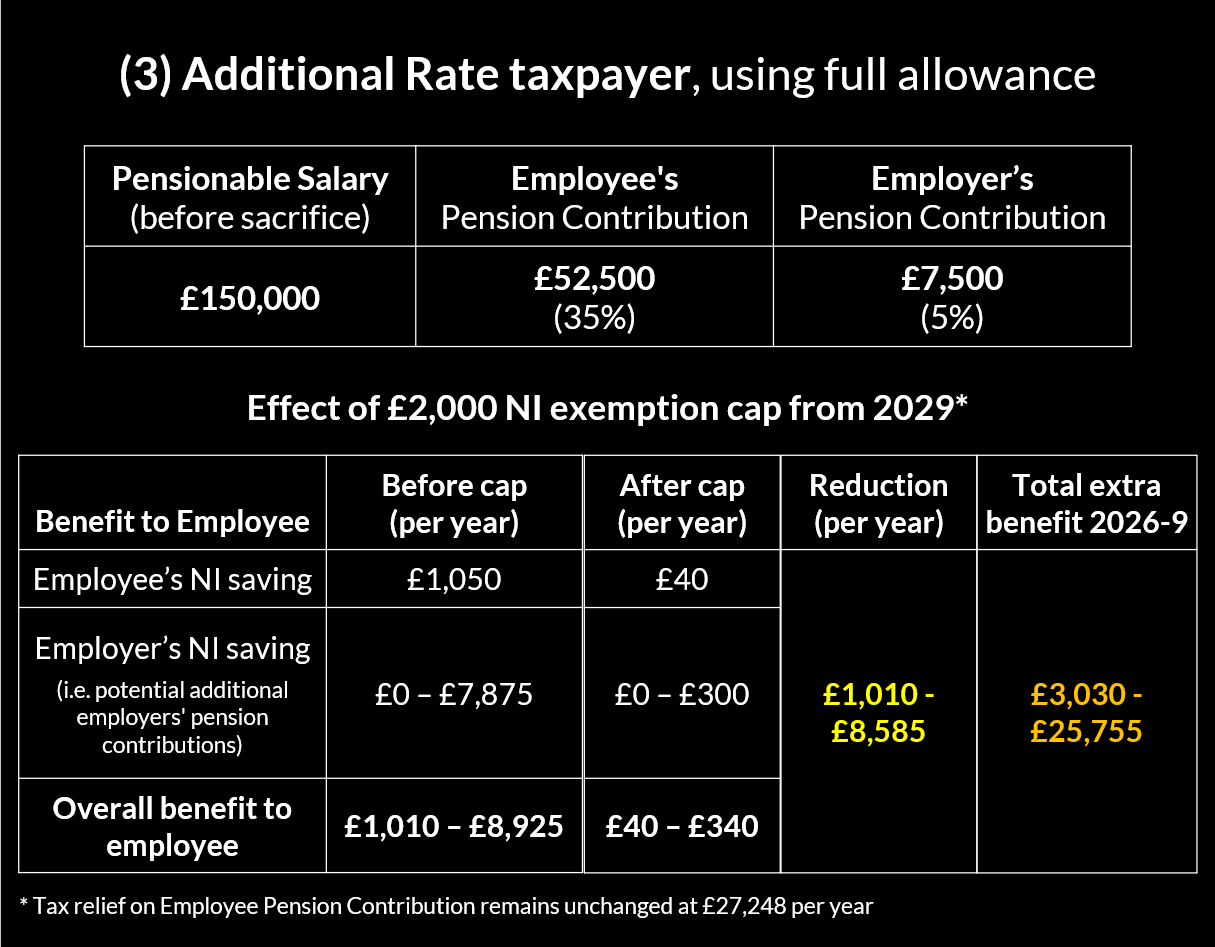

- Additional Rate taxpayer (£150,000 pensionable salary, contributing the full £60,000 annual allowance including £7,500 employer contributions via salary sacrifice): the current annual benefit is up to £8,925 — £1,050 in Employee NI saving plus up to £7,875 from employer NI sharing. After 2029, this collapses to up to £240 — a fraction of the current benefit, representing a very significant change for this group.

The higher the amount currently sacrificed above £2,000, the more dramatically the cap reduces the benefit. For Basic Rate and lower-Higher-Rate earners, the change is modest. For high earners maximising pension contributions, it is substantial.

What should you consider doing differently before and after the changes?

While April 2029 is still some years away, it is worth planning ahead — particularly if you currently sacrifice more than £2,000 per year or are a higher earner.

- Audit your current sacrifice level: calculate how much you sacrifice annually and whether it exceeds £2,000. For example, if you earn £60,000 and sacrifice 8% (£4,800), you will pay NI on £2,800 of that from 2029 — at 2% above the upper earnings limit, that is around £56 extra NI per year, modest but cumulative.

- Engage with your employer: ask how they intend to treat NI savings after April 2029 and whether their contribution matching formula will change.

- Re-optimise your contribution split: if you currently sacrifice more than £2,000, consider using salary sacrifice only up to the £2,000 limit for maximum NI efficiency, with any additional pension saving made via standard employee contributions. This approach still attracts full income tax relief, and avoids unnecessarily reducing your contractual salary — which can otherwise lower employment benefits linked to pay (such as life cover) and reduce your mortgage borrowing capacity with lenders who use a multiple of basic salary.

- Check whether your employer will still pass on NI savings on the first £2,000 of sacrifice, and how this interacts with any matching formula in your scheme rules.

- Keep your broader savings mix under review: for contribution amounts that would substantially exceed the cap, look beyond salary sacrifice to other tax-efficient options — ISAs, contributions into a spouse's or civil partner's pension, or taxable investments — once you have optimised your pension and NI advantages, considering your tax bands now and expected in retirement. This is especially relevant for higher earners who previously used salary sacrifice to make very large pension contributions.

- Seek personalised advice if your income is high, your contributions are large, or you are close to key thresholds — particularly the £100,000 personal allowance taper, the Child Benefit charge range, or the annual allowance limit. The interaction between salary sacrifice, NI, and these thresholds is complex enough that tailored cashflow planning can make a meaningful difference to outcomes.

Final thoughts: will salary sacrifice still be worth it?

The changes do not make salary sacrifice a poor strategy — for the majority of employees contributing modest amounts, the benefits remain largely intact. However, salary sacrifice is no longer the powerful optimisation tool it once was—especially for higher earners. The key is ensuring your contribution structure is optimised for the new rules, and that broader retirement saving decisions are reviewed in light of the reduced advantage at higher contribution levels.

For most people, the best approach going forward will be:

- Optimise employer contributions and matching

- Use salary sacrifice up to the £2,000 NI-free limit

- Supplement with other tax-efficient investments

As with all financial planning decisions, the right strategy depends on your individual circumstances, goals, and long-term tax position.

Happy Planning!

You can get a view of your projected long-term tax position by creating your own lifetime financial plan, made possible by the MyFinanceFuture Planner - a professional-level cashflow planning tool now available to consumers. The Planner allows you to understand the impact of the Budget's changes on your plans, and get a view of your likely tax band in retirement as input to pension savings decisions. It also gives you a basis for your long-term financial decisions and helps bring peace of mind that you have a financial plan in place for your future. Why not try it today by signing up for MyFinanceFuture Planner's free, Basic service - no credit card required - and find out if financial planning could help you?

MyFinanceFuture Services Ltd does not offer regulated financial or professional advice.

If you have questions or feedback on the content of this post, please contact us here.

LAUNCH THE PLANNER

LAUNCH THE PLANNER